Obama’s Deficit Reduction Plan Has Room for Improvement

9/27/2011

The nation is less than two months away from what could be a seminal moment in its fiscal history. In late November, the new “Super Committee,” formed by the recent debt ceiling deal, will release its set of recommendations to cut the federal budget deficit by $1.2 trillion. In an effort to influence the hectic debate the committee’s recommendations are sure to start, President Obama released on Sept. 19 a $3.3 trillion deficit reduction plan as a package of recommendations for the committee to adopt.

The nation is less than two months away from what could be a seminal moment in its fiscal history. In late November, the new “Super Committee,” formed by the recent debt ceiling deal, will release its set of recommendations to cut the federal budget deficit by $1.2 trillion. In an effort to influence the hectic debate the committee’s recommendations are sure to start, President Obama released on Sept. 19 a $3.3 trillion deficit reduction plan as a package of recommendations for the committee to adopt.

While the president’s recommendations are probably more progressive than any plan the committee will produce, they leave room for improvement, especially on the revenue side. The president’s recommendations include 28 separate tax provisions, totaling $1.6 trillion, with many only accruing a few billion dollars over the next ten years.

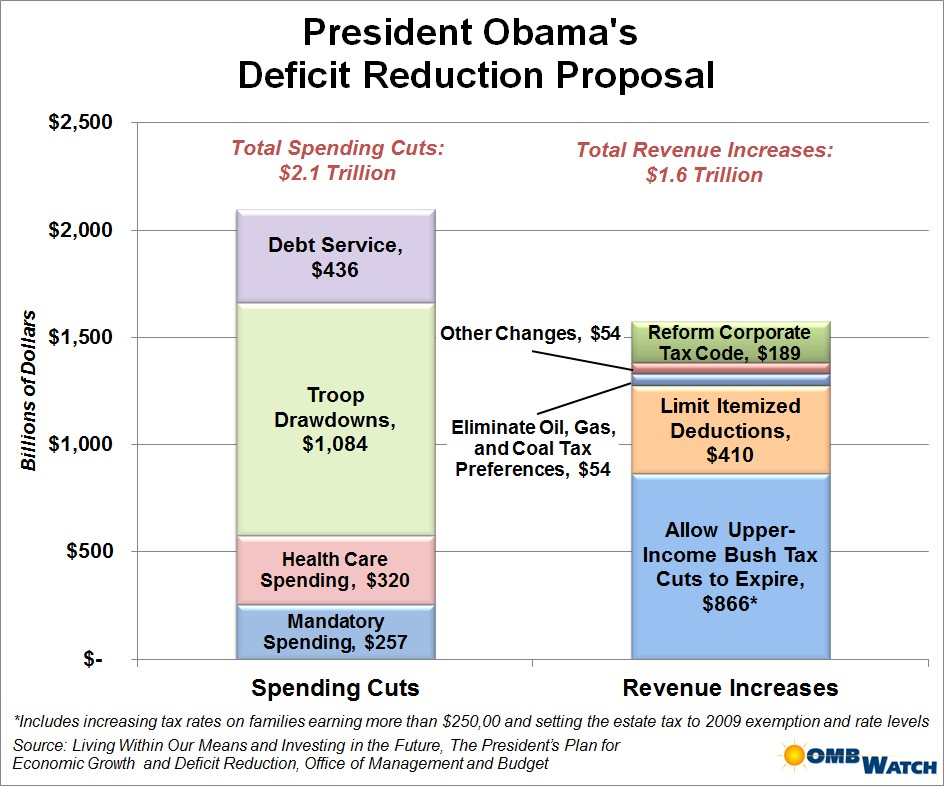

By far the largest tax provision in Obama’s plan is the expiration of the upper-income Bush tax cuts (including returning the estate tax to 2009 levels). This reduces the deficit by $866 billion over ten years, more than half of the total revenue that the plan would collect. The president’s proposal would return the top two tax brackets to their late-1990s levels of 36 percent and 39.6 percent, an increase of about three percentage points for each bracket. These changes would only affect families earning about $250,000 per year or more. The middle-income tax cuts, however, would remain untouched, making the entire tax code more progressive overnight.

Another quarter of the president’s revenue comes from limiting the benefit of itemized deductions on upper-income taxpayers. This is a broad change that would affect many well defended tax breaks, including the home mortgage interest deduction, the charitable giving deduction, and certain medical expenses, but without specifically targeting any particular item. Currently, the deductions are worth whatever a taxpayer’s top marginal tax rate is, since itemized deductions simply lower a taxpayer’s taxable income. (For example, someone in the 35 percent bracket who gives $100 to her favorite charity would see a $35 tax benefit, whereas someone in the 28 percent bracket would see a $28 benefit.). The recommendations limit the benefit of these deductions to 28 percent of a taxpayer’s income for taxpayers in the top two brackets, essentially “leveling off” the benefit after the third-highest bracket, but it would not cap the total amount of itemized deductions a taxpayer can claim. In other words, taxpayers who currently see a deduction of 35 cents of every donated dollar would receive only a 28-cent benefit, or a 20 percent decrease. This change, while seemingly small, would bring in $410 billion over the next ten years.

The president’s recommendations generate another $110 billion over ten years by closing three complicated corporate tax loopholes. Two of the loopholes, the so-called “last-in, first out” (LIFO) and “lower-of-cost-or-market” (LCM) loopholes, are accounting maneuvers that businesses can use to game the costs of their inventories in order to inflate their deductions. By closing these two loopholes, the president’s plan would save about $60 billion over ten years. The third loophole involves the foreign tax credit, which Obama proposes to determine on a “pooling” basis, or based on the consolidated earnings and profits and foreign taxes of all of a company’s foreign subsidiaries. Changing the credit to a pooling basis would save the nation about $53 billion over the next decade. (Note that these three provisions are a subset of the green bar labeled "Reform Corporate Tax Code" in the accompanying chart.)

Notably absent from the list of revenue provisions is reference to the “Buffett Rule,” which is named after billionaire financier Warren Buffett and which holds that households making over $1 million a year should not pay a smaller share of their income in taxes than middle-class families. While this rule has received a great deal of attention in the news, the president’s plan only includes this as a principle, not a specific policy provision. Instead, Obama hopes that his changes will help make the tax system fairer and closer to complying with the Buffett Rule.

(Click to enlarge)

While a great deal of the president’s deficit reduction comes from tax increases on high-income earners, Obama’s plan would also cut $1.7 trillion in spending. The plan assumes $1.1 trillion in savings from troop reductions in Iraq and Afghanistan and $600 billion in spending reductions from almost 60 different health care and mandatory program policy changes. Of the $600 billion in domestic spending cuts, the president recommends saving some $257 billion from assorted mandatory programs, such as eliminating direct payments to farmers ($30 billion over ten years), and another $320 billion would come from health care programs, most prominently Medicare and Medicaid. About $135 billion of the health savings comes from allowing Medicare Part D low-income beneficiaries to benefit from the same rebates Medicaid receives for name-brand and generic drugs.

Although a good portion of the health care savings avoids reducing benefits, the billions of dollars in benefit reductions that are proposed would impact low-income families and retirees. The Super Committee could mitigate these impacts by generating a plan that produces additional revenues instead of proposing cuts. One popular alternative is a financial speculation tax, which would charge a small fee on each stock transaction in an effort to discourage short-term, high-volume speculation. Many other countries, even some with flourishing financial centers such as Great Britain, have a similar tax, and the United States had one until the late 1960s. Two polls from 2010 suggest that a majority of Americans would support some kind of a financial speculation tax.

The organization Our Fiscal Security estimated in 2010 that a 0.5 percent tax per transaction would raise about $77 billion per year. Others have estimated a broad financial speculation tax could raise $130 billion per year. Over ten years, a financial speculation tax would decrease the deficit far more than any of the mandatory savings proposed in the president’s plan, and the tax has the added incentive of having a positive policy outcome (less volatility in trading).

Taxing capital gains and dividends as ordinary income could be another source of revenue. Currently, these forms of income are taxed at a lower rate than some wages, creating preferential treatment for a source of income derived from wealth. By repealing the 15 percent rate for capital gains and dividends, and instead taxing it according to the normal income tax rates, the nation could bring in $918 billion over the next decade while making the tax code fairer.

The president could also recommend instituting a wealth surtax instead of the mandatory cuts. A wealth surtax, such as a tax bracket for millionaires, would make the tax code more progressive. The past decade has seen a marked increase in wealth in the upper reaches of society, while low- and middle-class wages have stagnated. Creating a wealth surtax could raise as much as $750 billion in the next ten years, ensuring that any deficit reduction is balanced and fair.

Any of these three options would make the president’s recommendations to the Super Committee more progressive. They would more than replace the mandatory and health care cuts in Obama’s current plan. The extra funding could even help undo some of the harmful discretionary cuts agreed to as part of the recent debt ceiling deal.