The Recovery Act Spending That Wasn't There

1/12/2010

Recovery Act recipient reporting has received a great deal of attention in the media, and while some of this coverage has been critical (reporting on non-existent congressional districts or ZIP codes, unreliable job creation numbers, etc.), many news articles portray comprehensive oversight of the act because of transparency requirements in the law. However, approximately two-thirds of the spending in the Recovery Act bypasses these requirements, leading to a dearth of information about how the money is being spent. As time passes and Recovery Act spending continues, this lack of data is becoming more apparent, as highlighted by a recent Internal Revenue Service (IRS) report showing that millions of dollars in Recovery Act tax breaks are vulnerable to tax fraud.

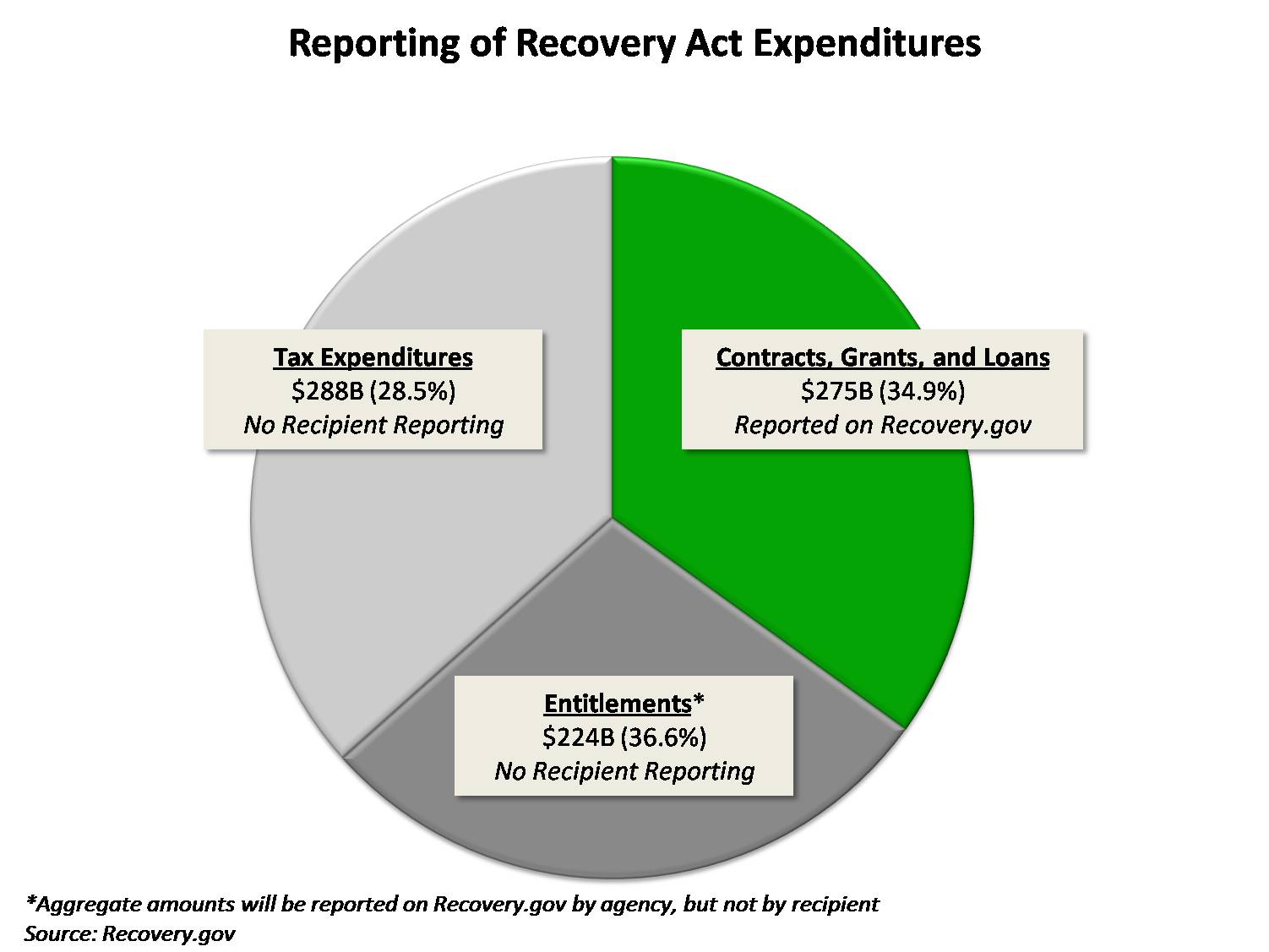

About one-third of Recovery Act spending, the discretionary funding, is subject to the tight reporting requirements and provides monetary resources for infrastructure, research, green energy, and other projects. Recipients of discretionary spending must report to the federal government on the use of their funds, reports which can be found on Recovery.gov and OMB Watch’s FedSpending.org. These reports provide unprecedented details on federal spending, containing information on recipient location, place of performance, a project description, number of jobs created, and the five highest-paid employees.

The other two-thirds of Recovery Act spending include entitlement spending and tax expenditures. Entitlements are direct payments to people, such as unemployment insurance, COBRA health insurance benefits, and one-time Social Security payments; tax expenditures are the tax credits and deductions authorized by the act. Congress exempted these entitlement payments and tax cuts from the Recovery Act reporting requirements largely for privacy reasons. This means that recipients of unemployment benefits or the Making Work Pay tax credit, for instance, do not report any information to Recovery.gov, and none is displayed.

(click to enlarge)

Accordingly, there is little information available on Recovery Act tax expenditures or entitlement spending, making debate on spending efficacy difficult. As policy experts and lawmakers vigorously debate the effect of the discretionary spending – thanks to the more than 130,000 recipient reports on discretionary spending released in October – they remain largely silent on the effectiveness of tax expenditures and entitlement spending.

One recent report helped highlight this disparity. In November 2009, the Treasury Inspector General for Tax Administration (TIGTA), the inspector general for the IRS, released a report warning that the IRS does not know if the $288 billion in Recovery Act tax expenditures are being claimed legitimately and cannot know without extensive auditing.

The problem is that the IRS did not require additional documentation for the new credits and deductions. For instance, the Recovery Act provides funding for the First-Time Homebuyer Credit, which provides a fully refundable $8,000 tax credit for first-time homebuyers, but the IRS does not require additional documentation for this credit, such as a HUD Settlement Statement, nor does it check the return against any third-party source, such as a housing database. Tax filers can claim the housing credit without providing any proof that they actually have purchased a house or even that a purchased house is a first-time purchase for the taxpayer. The only way the IRS can catch such fraudulent claims is through an audit.

The IRS claims requiring documentation on tax credits and deductions is too "burdensome" on businesses and individuals, because filing documentation precludes electronic filing; the IRS notes that this would prevent some two million First Time Homebuyer Credit claimants from filing electronically. But detecting fraud after federal funds have been disbursed (i.e., through an audit instead of before a return is processed) usually results in a lower rate of return on tax enforcement, since audits are a lengthy and relatively costly process compared to requiring upfront documentation.

This problem exists because Congress did not enact any transparency provisions for the tax expenditures and entitlement spending. The lack of transparency and accountability provisions in these sections of the Recovery Act is apparent now that the first round of recipient reports has been released. While Recovery.gov users can track the precise details of some $275 billion in discretionary spending, down to the location of the material suppliers for some projects, next to nothing is known about the recipients of the remaining two-thirds of Recovery Act spending.

The privacy rights of citizens should be protected, but more information on Recovery Act tax expenditures and entitlement spending is needed. Currently, there is very little information available, and accordingly, little debate. The TIGTA report caused little reaction outside of a few, tax policy-focused blogs. The most attention the issue received was in the form of a short New York Times article, published almost a month after TIGTA released the report. Additional data, if available, would help shed light on how this money is being used.